The End of an Era—and to New Beginnings

Download the full PDF here.

It is the end of an era: after 60 years at the helm, one of the world’s most closely watched investors has stepped down as CEO.

Very few people stay in one role for six decades. For context, the median tenure with a single employer dropped to 3.9 years in the U.S., while the average working life spans roughly 37 years.1 This puts into perspective the remarkable length of Warren Buffett’s leadership of Berkshire Hathaway—nearly twice the span of a typical career.

Even if you don’t subscribe to Buffett’s investing philosophy, the scale of his accomplishments is clear. After taking control in 1965, he transformed Berkshire from a struggling textile mill into a multi-national conglomerate holding company, growing its share price from about $19 to roughly $745,000—a cumulative gain of nearly 4,000,000 percent! In 2024, Berkshire became the first U.S. non-tech company to surpass a trillion-dollar market capitalization.

Now 95, Buffett shared in November that he was “going quiet”2 and will no longer write the annual letter or speak at Berkshire’s annual meeting. In his farewell, he offered reflections on both business and life.3 As we begin a new year, several insights may serve as practical reminders for our own wealth management:

Succession planning takes time. Greg Abel, named as Buffett’s successor in 2021, has been groomed for many years, spending nearly three decades at Berkshire and rising to Vice Chairman in 2018. Even after the transition, Buffett plans to “keep a significant amount” of his shares until shareholders gain confidence in Abel’s leadership.

Estate planning is fluid. Buffett has revised his estate plan many times over the years. His “unexpected longevity has unavoidable consequences” as his three children are now beyond retirement age (72, 70 and 67). He now aims to accelerate lifetime gifts to their foundations so they can fulfill his goal of distributing his entire estate while they’re alive.

Markets go up and down. While market returns have been strong in recent years, Buffett reminds us that markets—and economies—will see difficult times: “Our stock price will move capriciously, occasionally falling 50 percent or so as has happened three times…under present management. Don’t despair; America will come back, and so will Berkshire shares.”

Our time is limited. “Father Time…is undefeated; for him, everyone ends up on his score card as wins,” Buffett notes. His advice? “Decide what you would like your obituary to say and live the life to deserve it.”

Buffett has long emphasized that money is a tool, not a purpose: “Greatness does not come about through accumulating great amounts of money, great amounts of publicity or great power in government.” Despite his accomplishments, Buffett distills success into something far simpler: “When you help someone in any of thousands of ways, you help the world. Kindness is costless but also priceless.”

Indeed, Buffett’s humility appears to have deepened with age. He acknowledges the role of luck in his successes—and the successes of many others—and admits he’s fallen short of his own ideals many times before: “I have been thoughtless countless times and made many mistakes but became very lucky in learning from some wonderful friends how to behave better.” His reminder: “The cleaning lady is as much a human being as the Chairman.”

And now, as he retires into the Chairman role, Buffett signs off with a message well-suited for a new year: “Choose your heroes very carefully and then emulate them. You’ll never be perfect, but you can always be better.”

As we turn the page to 2026, here’s to a new year that inspires reflection, growth and purpose—and, as in Buffett’s case, new beginnings. Happy New Year!

- https://www.bls.gov/news.release/pdf/tenure.pdf

- “Sort of”: he will pen an annual Thanksgiving message.

- https://www.berkshirehathaway.com/news/nov1025.pdf

financial resolution Time

For 2026: Make Estate Planning a Priority

Happy 2026! If improving your financial well-being is on your list of New Year’s resolutions, a great place to start is with your estate plan. A comprehensive plan ensures your assets are distributed according to your wishes, while helping to maximize the legacy you leave behind.

If you already have an estate plan in place, here are five questions to ask that may prompt a review:

- Does my plan promote efficient administration and limit unnecessary expenses?

- Will my plan minimize family effort—or even potential conflict?

- Are my assets protected from potential liabilities, such as former spouses or creditors?

- Do I have safeguards in place to allow my family to make financial and healthcare decisions if I am unable?

- Can my family maintain their current lifestyle if I am no longer able to contribute?

Minimizing Taxes & Fees

A key goal of many estate plans is to reduce taxes and other fees. For Canadian income tax purposes, most assets—including real property and shares—are deemed to be disposed of immediately prior to death and may be subject to tax, except where certain exceptions, such as spousal rollovers, apply. Some provinces also charge probate fees, which can vary significantly. Additionally, Canadians holding U.S. situs assets, such as shares of U.S. corporations or U.S. real estate, may need to plan for potential U.S. estate tax.

While taxes and fees can create a substantial obligation for many estates, careful planning can help reduce or defer them. This may be as simple as arranging bequests differently, using life insurance to help cover tax liabilities or, for business owners, leveraging tools such as an estate freeze or the Lifetime Capital Gains Exemption to ease succession planning.

It’s More Than Just Finances

A comprehensive estate plan goes beyond maximizing the estate value passed to beneficiaries. It can also ensure fairness among heirs or protect those who may need guidance in managing assets. Trusts, for example, can help preserve assets for beneficiaries who cannot manage them independently or prevent access by creditors. By planning ahead, you can create a lasting foundation that reflects your values and helps your legacy endure across generations.

Why Not Make Estate Planning a Priority in 2026?

Like many things in life, estate planning can easily fall down the priority list. For some, the subject feels unsettling, perhaps a reminder of our own mortality. For others, it simply gets lost in the bustle of daily life. Yet establishing a basic plan, and keeping it updated as circumstances change, is one of the greatest gifts you can give to your loved ones.

Being familiar with the many aspects of your financial situation, we can provide guidance, counsel or recommendations for experts in the field to assist with your estate plan.

looking below the surface

Equity Market Perspectives: Growth Is Expected to Continue

After equity markets continued to reach new highs in 2025, there have been renewed concerns about elevated valuations. Are stock prices outpacing underlying fundamentals, or is there still room to run?

Many factors influence market performance—government policies, geopolitical events, economic growth, inflation, interest rates and even the headlines. Yet over the long run, one of the most powerful drivers is corporate earnings.

The earnings story, so far, has been strong. U.S. corporate margins have expanded, with the average S&P 500 net income margin climbing above 10 percent this decade, roughly double the level of the 1990s. Canadian corporate profits have followed a similar trajectory, though fluctuations in commodity prices, including a pronounced peak in 2022, have added more volatility to overall profits.

Looking ahead, several factors suggest that this growth can continue. Companies are benefiting from technological innovation, productivity gains and resilient consumer demand, all of which support sustained earnings growth. Of course, history reminds us that earnings growth alone doesn’t guarantee high market returns. In the 1970s, despite solid earnings growth of 9.9 percent, high inflation and the global energy shocks kept equity markets subdued. Indeed, growth in markets, economies—and even human progress—is rarely linear.

Even so, the current strength in earnings should not be overlooked. Robust corporate profits have been, and remain, a key driver of market strength. As we look ahead to 2026, here’s to continued earnings growth to provide the fuel for markets to keep advancing.

S&P 500: Key Drivers of Stock Market Performance

| Decade |

Dividends |

Earnings Growth |

P/E Change |

Annual Returns |

| 1970s |

3.5% |

9.9% |

-7.5% |

5.9% |

| 1980s |

5.2% |

4.4% |

7.7% |

17.3% |

| 1990s |

3.2% |

7.4% |

7.2% |

17.8% |

| 2000s |

1.2% |

0.8% |

-3.2% |

-1.2% |

| 2010s |

2.0% |

10.6% |

1.0% |

13.6% |

| 2020s |

1.5% |

9.0% |

3.9% |

14.4% |

Legendary investor John Bogle once suggested the key drivers of equity returns are dividend yield, earnings growth and speculative return or changes in valuations (the price/earnings (P/E) change). Source: “Don’t Count on It,” J. Bogle; https://awealthofcommonsense.com/2025/10/animal-spirits-why-retail-is-outperforming/

RRSP Season IS HERE AGAIN

The RRSP: Why Are We Falling Short? Debunking Two Myths

While many of us are unhappy about the high taxes we pay, one way to ease the burden is by fully using tax-advantaged accounts. Yet RRSP participation rates have declined over the past two decades, from 29.1 percent of taxpayers in 2000 to just 21.7 percent in 2022. The good news: high-income earners are more likely to contribute: 66 percent of taxpayers earning between $200,000 and $500,000 contributed in 2023. But younger Canadians are falling short. The introduction of the Tax-Free Savings Account (TFSA) in 2009 may be part of the reason, but persistent misconceptions about the RRSP also play a role. Let’s address two common myths:

Myth 1: It’s better to invest in a TFSA than an RRSP. In fact, the RRSP generally yields a greater benefit if you expect a lower tax rate in retirement. In practice, many contribute to their RRSP during higher-income working years and withdraw when income is lower in retirement, leading to an advantage for the RRSP. Of course, there may be situations when the TFSA is a better choice, such as if you have a higher tax rate at withdrawal or face recovery tax for income-tested benefits like Old Age Security.

Myth 2: RRSPs aren’t worth it because withdrawals are fully taxed, whereas in non-registered accounts, only income and gains are taxed. A common complaint is that RRSP withdrawals are fully taxed at marginal rates, whereas non-registered accounts only tax income and gains (with favourable tax treatment for dividends and capital gains). While it’s true that RRSP withdrawals (usually from a Registered Retirement Income Fund (RRIF)) are taxed as income, what’s often forgotten is the initial tax deduction at contribution. Remember: a $30,000 RRSP contribution is equivalent to an after-tax contribution of $18,000 at a marginal tax rate of 40 percent. If your tax rate is the same at the time of contribution and withdrawal, you effectively receive a tax-free rate of return on your net after-tax RRSP contribution (chart). In many cases, even if your tax rate is higher at the time of withdrawal, you may be better off compared to a non-registered account due to the effect of tax-free compounding over long time periods.

While the fair market value of the RRSP/RRIF at death is generally included in the terminal tax return and taxed at marginal rates, there may be ways to mitigate the potential tax liability. This includes a tax-deferred rollover to a spouse or financially dependent (grand)child. Another way to manage the potential tax bill is to engage in a “meltdown strategy,” making withdrawals earlier when your tax rate is lower than you expect in the future or at the year of death.

2026 Reminders for Tax-Advantaged Accounts

RRSP Deadline — The deadline for RRSP contributions for the 2025 tax year is Monday, March 2, 2026, limited to 18 percent of the previous year’s earned income, to $32,490 (for 2025).*

2026 TFSA Dollar Limit: $7,000, making the eligible lifetime contribution room $109,000.

*Plus any previous years’ unused contribution room carried forward, less any pension adjustments.

MACROECONOMIC PERSPECTIVES

In Brief: What Is the “K-Shaped” Economy?

The eleventh letter of the alphabet has taken on new meaning. The letter “K” is now used to describe the bifurcation in today’s economy. Different consumer segments and the businesses that serve them are growing at different rates. Indeed, there’s a divergence: The upward-slanting arm of the “K” represents higher-income households with strong consumer spending, fuelled by healthy income growth and rising wealth. In contrast, the downward-slanting arm represents low- and middle-income households facing rising living costs, stagnant wages and higher debt burdens.

Since consumer spending drives more than two-thirds of total U.S. GDP, this divide carries implications. Higher-income households are now responsible for a disproportionate share of economic activity. In Q2 2025, the top 10 percent of income earners accounted for nearly half of all U.S. consumer spending. This imbalance underscores how economic resilience has become concentrated among wealthier consumers—those benefiting most from asset price appreciation. As a result, the softer labour-market figures observed in 2025 that largely impacted lower-income households attracted less attention as they didn’t materially affect overall consumption.

Where are economies and markets headed in 2026? In 2025, artificial intelligence (AI) was a key driver of market enthusiasm. If AI capital investments deliver productivity gains, markets may look past ongoing labour-market weakness, effectively shrugging off the lower part of the K—although expectations may already be partly reflected in valuations. At the same time, monetary stimulus from interest rate cuts in Canada and the U.S., tariff renegotiations and potential U.S. tax refunds could strengthen labour markets and support more exposed sectors. Yet some argue the same stimulus has exacerbated wealth inequality.

As advisors, we continue to navigate the evolving landscape. The “K-shaped” economy reinforces the value of time-tested principles—diversification, a focus on quality and ongoing risk management—as key to successful long-term wealth management in an increasingly uneven economic environment.

Supporting otherS & YOURSELF

Estate Planning: Five Estate Executor Mistakes

Administering an estate can be a time-consuming and complex task, often made more challenging by emotionally difficult circumstances. All too often, executors can make mistakes that have the potential to lead to increased tax liabilities, conflict with or between beneficiaries or, worse yet, escalation to potential litigation. Equally concerning, the executor risks personal liability for these mistakes.

If you have been appointed to administer an estate, being aware of these potential pitfalls may help as you contemplate the role. As you plan for your own estate, carefully selecting your executor is important to prevent these and other mistakes.

Here are five common errors:

- Overlooking directives in the will. Estate lawyers suggest that executors can sometimes ignore parts of the will, such as forgiving loans that were to be collected, perhaps due to a lack of knowledge or because it is easy or convenient. Others may choose to distribute assets differently than directed within the will, under the belief that they have a more ‘fair’ idea for this distribution. However, neither situation is within an executor’s authority, exposing them to potential liability.

- Failing to communicate. Sometimes executors become so involved in the process that they neglect to communicate. One of the executor’s duties is to respond to reasonable enquiries from beneficiaries. Silence can often be misinterpreted as being secretive or suspicious, which can prompt estate disputes. Maintaining transparency and ongoing communication can go a long way in helping to prevent conflict.

- Making distributions too early. If distributions are made too early, such as before taxes or other liabilities are paid, the executor may be held personally responsible. This can often happen when the executor succumbs to pressure from beneficiaries for distributions. However, any outstanding debts of the deceased must be paid before estate assets can be distributed to beneficiaries—and it is the job of the executor to identify these debts. Sometimes the executor overlooks the importance of determining whether there are unknown creditors, which often involves a time-consuming process of creating a public notice. Advertising for creditors can protect the executor should a creditor make a claim after the estate has been distributed.

- Trying to keep costs low. Some executors may act too prudently in trying to limit estate expenses. However, this may lead to higher eventual costs. For example, if an executor decides to do the tax returns without the help of an accountant, they may miss eligible tax credits or deductions. In the past, advertising for creditors in the newspapers of multiple cities was very costly, so some executors avoided this process to save money, only to be caught by surprise when creditors eventually made claims.

- Treating estate funds as their own. Given the assets often available within an estate, some executors may wrongly use estate funds for their own purposes, such as to make loans to themselves or family members. Others may make more honest mistakes, such as using funds to cover travel costs for family members to attend the funeral. If estate funds are used incorrectly, the executor may be held personally liable. Additionally, if the executor acts unreasonably or in their own self-interest, they may not be entitled to compensation from the estate.1

As you support others, be aware of the responsibilities and potential pitfalls that come with serving as an executor. For more perspectives, or for an introduction to an estate planning specialist who can provide greater insight, please call the office.

- https://www.canlii.org/en/on/onca/doc/2016/2016onca521/2016onca521.html

The Role of an Executor: A Significant Responsibility

Not everyone may be well-suited to serve as an executor. Understanding what the role entails can help you decide whether to take on this responsibility. Keep in mind that it is a substantial commitment, which may include:

- Time commitment — settling an estate can take 18 months on average, or longer for more complex estates.

- Business judgment — the role often requires making informed financial and administrative decisions.

- Legal responsibility — there are important legal obligations associated with the position.

- Conflict management — you may need to navigate disagreements among beneficiaries.

- Residency considerations — your place of residence may have tax or legal implications for the estate.

Given these challenges, there may be value in considering the use of a professional executor to support the process.

Newswire

Quarterly Investment Insights – Winter 2026

The End of an Era—and to New Beginnings

Download the full PDF here.

It is the end of an era: after 60 years at the helm, one of the world’s most closely watched investors has stepped down as CEO.

Very few people stay in one role for six decades. For context, the median tenure with a single employer dropped to 3.9 years in the U.S., while the average working life spans roughly 37 years.1 This puts into perspective the remarkable length of Warren Buffett’s leadership of Berkshire Hathaway—nearly twice the span of a typical career.

Even if you don’t subscribe to Buffett’s investing philosophy, the scale of his accomplishments is clear. After taking control in 1965, he transformed Berkshire from a struggling textile mill into a multi-national conglomerate holding company, growing its share price from about $19 to roughly $745,000—a cumulative gain of nearly 4,000,000 percent! In 2024, Berkshire became the first U.S. non-tech company to surpass a trillion-dollar market capitalization.

Now 95, Buffett shared in November that he was “going quiet”2 and will no longer write the annual letter or speak at Berkshire’s annual meeting. In his farewell, he offered reflections on both business and life.3 As we begin a new year, several insights may serve as practical reminders for our own wealth management:

Succession planning takes time. Greg Abel, named as Buffett’s successor in 2021, has been groomed for many years, spending nearly three decades at Berkshire and rising to Vice Chairman in 2018. Even after the transition, Buffett plans to “keep a significant amount” of his shares until shareholders gain confidence in Abel’s leadership.

Estate planning is fluid. Buffett has revised his estate plan many times over the years. His “unexpected longevity has unavoidable consequences” as his three children are now beyond retirement age (72, 70 and 67). He now aims to accelerate lifetime gifts to their foundations so they can fulfill his goal of distributing his entire estate while they’re alive.

Markets go up and down. While market returns have been strong in recent years, Buffett reminds us that markets—and economies—will see difficult times: “Our stock price will move capriciously, occasionally falling 50 percent or so as has happened three times…under present management. Don’t despair; America will come back, and so will Berkshire shares.”

Our time is limited. “Father Time…is undefeated; for him, everyone ends up on his score card as wins,” Buffett notes. His advice? “Decide what you would like your obituary to say and live the life to deserve it.”

Buffett has long emphasized that money is a tool, not a purpose: “Greatness does not come about through accumulating great amounts of money, great amounts of publicity or great power in government.” Despite his accomplishments, Buffett distills success into something far simpler: “When you help someone in any of thousands of ways, you help the world. Kindness is costless but also priceless.”

Indeed, Buffett’s humility appears to have deepened with age. He acknowledges the role of luck in his successes—and the successes of many others—and admits he’s fallen short of his own ideals many times before: “I have been thoughtless countless times and made many mistakes but became very lucky in learning from some wonderful friends how to behave better.” His reminder: “The cleaning lady is as much a human being as the Chairman.”

And now, as he retires into the Chairman role, Buffett signs off with a message well-suited for a new year: “Choose your heroes very carefully and then emulate them. You’ll never be perfect, but you can always be better.”

As we turn the page to 2026, here’s to a new year that inspires reflection, growth and purpose—and, as in Buffett’s case, new beginnings. Happy New Year!

financial resolution Time

For 2026: Make Estate Planning a Priority

Happy 2026! If improving your financial well-being is on your list of New Year’s resolutions, a great place to start is with your estate plan. A comprehensive plan ensures your assets are distributed according to your wishes, while helping to maximize the legacy you leave behind.

If you already have an estate plan in place, here are five questions to ask that may prompt a review:

Minimizing Taxes & Fees

A key goal of many estate plans is to reduce taxes and other fees. For Canadian income tax purposes, most assets—including real property and shares—are deemed to be disposed of immediately prior to death and may be subject to tax, except where certain exceptions, such as spousal rollovers, apply. Some provinces also charge probate fees, which can vary significantly. Additionally, Canadians holding U.S. situs assets, such as shares of U.S. corporations or U.S. real estate, may need to plan for potential U.S. estate tax.

While taxes and fees can create a substantial obligation for many estates, careful planning can help reduce or defer them. This may be as simple as arranging bequests differently, using life insurance to help cover tax liabilities or, for business owners, leveraging tools such as an estate freeze or the Lifetime Capital Gains Exemption to ease succession planning.

It’s More Than Just Finances

A comprehensive estate plan goes beyond maximizing the estate value passed to beneficiaries. It can also ensure fairness among heirs or protect those who may need guidance in managing assets. Trusts, for example, can help preserve assets for beneficiaries who cannot manage them independently or prevent access by creditors. By planning ahead, you can create a lasting foundation that reflects your values and helps your legacy endure across generations.

Why Not Make Estate Planning a Priority in 2026?

Like many things in life, estate planning can easily fall down the priority list. For some, the subject feels unsettling, perhaps a reminder of our own mortality. For others, it simply gets lost in the bustle of daily life. Yet establishing a basic plan, and keeping it updated as circumstances change, is one of the greatest gifts you can give to your loved ones.

Being familiar with the many aspects of your financial situation, we can provide guidance, counsel or recommendations for experts in the field to assist with your estate plan.

looking below the surface

Equity Market Perspectives: Growth Is Expected to Continue

After equity markets continued to reach new highs in 2025, there have been renewed concerns about elevated valuations. Are stock prices outpacing underlying fundamentals, or is there still room to run?

Many factors influence market performance—government policies, geopolitical events, economic growth, inflation, interest rates and even the headlines. Yet over the long run, one of the most powerful drivers is corporate earnings.

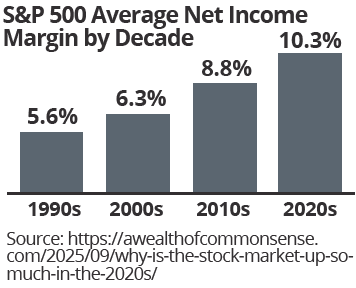

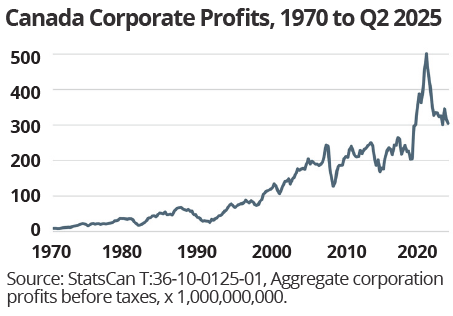

The earnings story, so far, has been strong. U.S. corporate margins have expanded, with the average S&P 500 net income margin climbing above 10 percent this decade, roughly double the level of the 1990s. Canadian corporate profits have followed a similar trajectory, though fluctuations in commodity prices, including a pronounced peak in 2022, have added more volatility to overall profits.

Looking ahead, several factors suggest that this growth can continue. Companies are benefiting from technological innovation, productivity gains and resilient consumer demand, all of which support sustained earnings growth. Of course, history reminds us that earnings growth alone doesn’t guarantee high market returns. In the 1970s, despite solid earnings growth of 9.9 percent, high inflation and the global energy shocks kept equity markets subdued. Indeed, growth in markets, economies—and even human progress—is rarely linear.

Even so, the current strength in earnings should not be overlooked. Robust corporate profits have been, and remain, a key driver of market strength. As we look ahead to 2026, here’s to continued earnings growth to provide the fuel for markets to keep advancing.

S&P 500: Key Drivers of Stock Market Performance

Legendary investor John Bogle once suggested the key drivers of equity returns are dividend yield, earnings growth and speculative return or changes in valuations (the price/earnings (P/E) change). Source: “Don’t Count on It,” J. Bogle; https://awealthofcommonsense.com/2025/10/animal-spirits-why-retail-is-outperforming/

RRSP Season IS HERE AGAIN

The RRSP: Why Are We Falling Short? Debunking Two Myths

While many of us are unhappy about the high taxes we pay, one way to ease the burden is by fully using tax-advantaged accounts. Yet RRSP participation rates have declined over the past two decades, from 29.1 percent of taxpayers in 2000 to just 21.7 percent in 2022. The good news: high-income earners are more likely to contribute: 66 percent of taxpayers earning between $200,000 and $500,000 contributed in 2023. But younger Canadians are falling short. The introduction of the Tax-Free Savings Account (TFSA) in 2009 may be part of the reason, but persistent misconceptions about the RRSP also play a role. Let’s address two common myths:

Myth 1: It’s better to invest in a TFSA than an RRSP. In fact, the RRSP generally yields a greater benefit if you expect a lower tax rate in retirement. In practice, many contribute to their RRSP during higher-income working years and withdraw when income is lower in retirement, leading to an advantage for the RRSP. Of course, there may be situations when the TFSA is a better choice, such as if you have a higher tax rate at withdrawal or face recovery tax for income-tested benefits like Old Age Security.

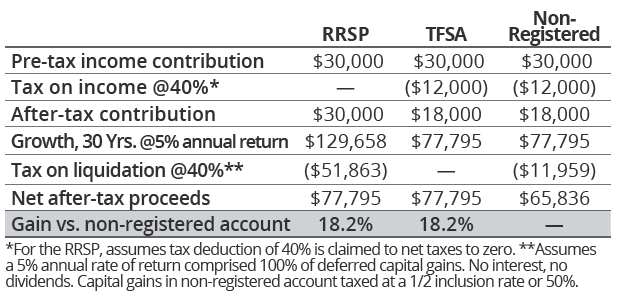

Myth 2: RRSPs aren’t worth it because withdrawals are fully taxed, whereas in non-registered accounts, only income and gains are taxed. A common complaint is that RRSP withdrawals are fully taxed at marginal rates, whereas non-registered accounts only tax income and gains (with favourable tax treatment for dividends and capital gains). While it’s true that RRSP withdrawals (usually from a Registered Retirement Income Fund (RRIF)) are taxed as income, what’s often forgotten is the initial tax deduction at contribution. Remember: a $30,000 RRSP contribution is equivalent to an after-tax contribution of $18,000 at a marginal tax rate of 40 percent. If your tax rate is the same at the time of contribution and withdrawal, you effectively receive a tax-free rate of return on your net after-tax RRSP contribution (chart). In many cases, even if your tax rate is higher at the time of withdrawal, you may be better off compared to a non-registered account due to the effect of tax-free compounding over long time periods.

While the fair market value of the RRSP/RRIF at death is generally included in the terminal tax return and taxed at marginal rates, there may be ways to mitigate the potential tax liability. This includes a tax-deferred rollover to a spouse or financially dependent (grand)child. Another way to manage the potential tax bill is to engage in a “meltdown strategy,” making withdrawals earlier when your tax rate is lower than you expect in the future or at the year of death.

2026 Reminders for Tax-Advantaged Accounts

RRSP Deadline — The deadline for RRSP contributions for the 2025 tax year is Monday, March 2, 2026, limited to 18 percent of the previous year’s earned income, to $32,490 (for 2025).*

2026 TFSA Dollar Limit: $7,000, making the eligible lifetime contribution room $109,000.

*Plus any previous years’ unused contribution room carried forward, less any pension adjustments.

MACROECONOMIC PERSPECTIVES

In Brief: What Is the “K-Shaped” Economy?

The eleventh letter of the alphabet has taken on new meaning. The letter “K” is now used to describe the bifurcation in today’s economy. Different consumer segments and the businesses that serve them are growing at different rates. Indeed, there’s a divergence: The upward-slanting arm of the “K” represents higher-income households with strong consumer spending, fuelled by healthy income growth and rising wealth. In contrast, the downward-slanting arm represents low- and middle-income households facing rising living costs, stagnant wages and higher debt burdens.

Since consumer spending drives more than two-thirds of total U.S. GDP, this divide carries implications. Higher-income households are now responsible for a disproportionate share of economic activity. In Q2 2025, the top 10 percent of income earners accounted for nearly half of all U.S. consumer spending. This imbalance underscores how economic resilience has become concentrated among wealthier consumers—those benefiting most from asset price appreciation. As a result, the softer labour-market figures observed in 2025 that largely impacted lower-income households attracted less attention as they didn’t materially affect overall consumption.

Where are economies and markets headed in 2026? In 2025, artificial intelligence (AI) was a key driver of market enthusiasm. If AI capital investments deliver productivity gains, markets may look past ongoing labour-market weakness, effectively shrugging off the lower part of the K—although expectations may already be partly reflected in valuations. At the same time, monetary stimulus from interest rate cuts in Canada and the U.S., tariff renegotiations and potential U.S. tax refunds could strengthen labour markets and support more exposed sectors. Yet some argue the same stimulus has exacerbated wealth inequality.

As advisors, we continue to navigate the evolving landscape. The “K-shaped” economy reinforces the value of time-tested principles—diversification, a focus on quality and ongoing risk management—as key to successful long-term wealth management in an increasingly uneven economic environment.

Supporting otherS & YOURSELF

Estate Planning: Five Estate Executor Mistakes

Administering an estate can be a time-consuming and complex task, often made more challenging by emotionally difficult circumstances. All too often, executors can make mistakes that have the potential to lead to increased tax liabilities, conflict with or between beneficiaries or, worse yet, escalation to potential litigation. Equally concerning, the executor risks personal liability for these mistakes.

If you have been appointed to administer an estate, being aware of these potential pitfalls may help as you contemplate the role. As you plan for your own estate, carefully selecting your executor is important to prevent these and other mistakes.

Here are five common errors:

As you support others, be aware of the responsibilities and potential pitfalls that come with serving as an executor. For more perspectives, or for an introduction to an estate planning specialist who can provide greater insight, please call the office.

The Role of an Executor: A Significant Responsibility

Not everyone may be well-suited to serve as an executor. Understanding what the role entails can help you decide whether to take on this responsibility. Keep in mind that it is a substantial commitment, which may include:

Given these challenges, there may be value in considering the use of a professional executor to support the process.

Recent Posts

June Market Insights: America at 250

The American 250th anniversary marks a new declaration. In his June Market Insights, James Thorne explores America’s rebirth—and why investors are not seeing the last gasp of U.S. exceptionalism.

May Market Insights: Mastery and the Terror Premium

As Brent trades above US$100, the hidden tax on energy is once again visible. In his May Market Insights, James Thorne explains why the U.S.-led operation against Iran could neutralize a nascent nuclear threat, reset oil toward US$60, and unlock a long deferred peace dividend.

April Market Insights: Bretton Woods 2.0, The New Great Game, and Trump

The New Great Game is taking shape—a U.S.-China rivalry over energy, AI infrastructure, and the dollar. In his April Market Insights, James Thorne weighs in on Bretton Woods 2.0, King Dollar, and what it means for investors.

March Market Insights: There is no Bronze Medal

The capex surging into AI looks less like froth and more like strategic reconstruction. In his March Market Insights, James Thorne explores how this capex supercycle is reshaping U.S. economic expansion—and why markets may be getting this key aspect of the AI story wrong.

February Market Insights: Fortress America and the Colony Next Door

The Trump Doctrine envisions a sovereign, American-led Western Hemisphere. But where does that leave Canada—and how do we secure our own economic sovereignty? James Thorne shares his thoughts in his February Market Insights.

The opinions contained herein are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Wellington-Altus Private Wealth. Assumptions, opinions and information constitute the author’s judgement as of the date this material and subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Graphs and charts are used for illustrative purposes only and do not reflect future values or future performance of any investment. The information does not provide financial, legal, tax or investment advice. Particular investment, tax, or trading strategies should be evaluated relative to each individual’s objectives and risk tolerance. All third party products and services referred to or advertised in this presentation are sold by the company or organization named. While these products or services may serve as valuable aids to the independent investor, WAPW does not specifically endorse any of these products or services. The third party products and services referred to, or advertised in this presentation, are available as a convenience to its customers only, and WAPW is not liable for any claims, losses or damages however arising out of any purchase or use of third party products or services. All insurance products and services are offered by life licensed advisors of Wellington-Altus.