Big Events in Calgary

Celebration for the Arts: This annual event at Jack Singer Concert Hall on May 4 continues to be a cherished tradition of honouring the artists and arts organizations that shape our city and recognizing outstanding achievements.

For more information, visit Celebration of the Arts.

YYC Italian Wine Fest: Visit Bridgeland’s Community Association on May 30 to celebrate Italian wine, food and culture Calgary style. Sip your way through Italy with bold reds, refreshing whites, and everything in between, each thoughtfully paired with Italian‑inspired dishes that keep the tasting experience going strong.

To learn more, visit YYC Italian Wine Fest.

EXECUTIVE SUMMARY

Reflection and Outlook

Family Office

REFLECTION AND OUTLOOK

The first quarter of 2026 reminded investors that markets rarely move in a straight line. The year began on firmer footing than many expected with economic growth holding up, employment remaining stable, inflation continuing to ease from prior highs and markets positive heading into March. North American central banks also held rates steady, reflecting an economy that is no longer running hot, but is still progressing.

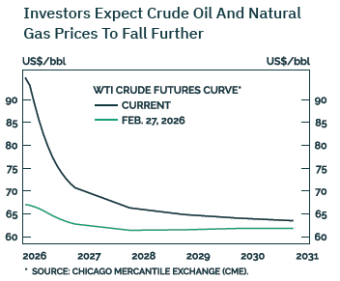

March, however, introduced a period of volatility once the U.S. and Israel waged war against Iran. The conflict drove energy prices higher, which in turn lifted inflation expectations and led markets to reassess the path of interest rates. This resulted in a broad market pullback, including both global stocks and bonds, particularly in areas that had previously led performance.

The quarter also reinforced the importance of diversification. While U.S. markets experienced a more pronounced decline, Canadian and international markets demonstrated greater resilience. During this period of volatility, our portfolios have been well supported due to our tactical allocation, particularly a meaningful tilt toward Canadian and international equities and exposure to energy and financial sectors.

In the short term, we believe there is a reasonable path toward de-escalation in the Iran conflict. Both sides have incentives to limit the duration of the disruption, particularly given the economic and political pressures associated with sustained elevated energy prices. With U.S. midterm elections approaching in November 2026, the incentive to stabilize conditions is increasing. While timing is uncertain, the likelihood of a prolonged and escalating conflict appears limited.

Over the longer term, the current environment is likely to drive several structural trends. There is increasing focus on energy security, which supports continued investment in oil and gas infrastructure, alongside renewables and nuclear energy. At the same time, global defence spending is expected to rise, and capital will continue to flow toward real assets and essential industries. These are not headwinds, but evolving opportunities we are considering best to take advantage of.

Our portfolios were intentionally positioned ahead of this environment. They remain well diversified and positive year to date despite the March correction. A balanced allocation across global stocks, private credit, and high-quality fixed income continues to provide stability, growth, and income. This positioning allows us not only to manage through volatility, but to take advantage of it.

We continue to view the current environment as light turbulence during a flight—noticeable, but not a change in direction. Periods like this create opportunities for disciplined investors. Our focus remains on thoughtful rebalancing, selectively adding to areas with improved valuations and income potential, and maintaining a long-term perspective. We remain confident in both the portfolios and the process behind them. Volatility is part of investing, but it also creates opportunity. Our role is to stay disciplined, act when opportunities arise, and ensure portfolios remain well positioned for the months and years ahead.

FAMILY OFFICE FEATURE:

The Family Cottage: Preserving Legacy

For many families, a cottage is rarely just a recreational property. It is often a multi‑generational asset—rich in history, emotion, and expectation. Yet cottages remain one of the most common sources of estate friction. Without careful planning, even a well‑intentioned legacy can result in avoidable costs and lasting family tension. Here are a few important things to keep in mind.

Capital Gains: A Known Liability That Requires Precision

Under Canadian tax law, a cottage is subject to a deemed disposition at the last death of a spouse, triggering capital gains tax on accumulated appreciation. For long‑held properties, even though only 50% of the gain is taxable, the tax can be substantial.

While the Principal Residence Exemption (PRE) may be used to shelter some or all of the gain, its application is nuanced. Only one property per year can be designated, and allocating the PRE to the cottage reduces the exemption available for other high‑value residences. For families with multiple properties, optimizing the PRE requires careful consideration.

Equality Versus Fairness Among Heirs

Cottages introduce emotional complexity that traditional estate planning does not easily solve. Some family members may have a deep attachment to the property and actively use it; others may see it primarily as a balance‑sheet asset. Treating all children “equally” can inadvertently feel unfair.

Some families may consider allocating the cottage to those who genuinely value stewardship and equalize the others with cash, other assets or insurance. The critical factor is clarity—both financial and emotional—well before the property changes hands.

Ownership Structure Matters

How the cottage is owned has long‑term consequences:

There is no default “best” structure—only what aligns with the family’s goals, risk tolerance, and time horizon.

Governance: The Real Determinant of Success

Where a cottage will be shared across generations, governance deserves the same rigour as a private family enterprise. A well‑drafted cottage agreement can address usage rights, cost allocation, decision‑making authority, capital improvements, dispute resolution, and exit mechanisms.

Planning Beyond Death

Incapacity planning is frequently overlooked. Enduring Powers of Attorney should explicitly authorize the management, maintenance, and insurance of recreational properties. Separate Powers of Attorney are also required in each province or state where you own property.

How We Help

For most families, cottage planning is a strategic exercise. We work with families to model current and long‑term tax exposure, design ownership and governance structures, and integrate cottage planning with broader estate and succession objectives. We also help document the reasons behind the owners’ intentions for the property and future generations. The goal is not merely to pass along a property, but to preserve a legacy in a way that is tax‑efficient, legally sound, and aligned with family values.

A cottage can be a unifying asset—or a quiet source of conflict. The difference is deliberate planning, done early and done well.

INVESTMENT MANAGEMENT FEATURE:

Private Credit: Near Term Headwinds vs. Long Term Resilience

Over the last two years, we have been investing in Private Credit within the portfolios we manage. We look at private credit as an alternative to fixed income/safe bonds. It provides a higher yield and overall return with only a slightly higher risk profile. Our expectation is for high-single-digit rates of return that are consistent and predictable and for portfolio returns to be enhanced in a more meaningful way than safe bonds have been able to provide over the past number of years.

Recently, there have been some less than favourable headlines related to private credit investments. We thought it would be helpful to provide a bit of an overview and to articulate that the private credit investments we use in portfolios are very conservative in nature, and as a result are very well positioned to take advantage of the opportunities arising from the dislocations in the space that have come about.

Twenty Years of Results Speak for Themselves

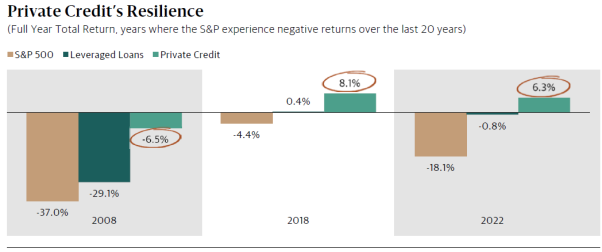

Below are some data points from a private credit index tracking firm called Cliffwater. Since 2004, private credit investments have returned roughly 9.5% per year, with only one down year (2008). These are the consistent results that led us to begin investing in the space. [1]

Manager Selection is Critical

Another reason we began investing in private credit was due to the advent of large, well recognized U.S. investment firms coming to Canada for the first time with private credit investment funds. These firms are among the largest private credit managers in the world with long track records of providing consistent returns in the high-single-digit range.

These firms invest on behalf of large insurance companies and pension plans, both government and private businesses. They have significant resources and scale that many Canadian managers do not, which, along with their tenure, size, and track-record, allow for a much more compelling risk-adjusted-return investment opportunity.

Private Credit in the News

You may have noticed recent headlines about fractures in the private credit space, particularly around increased investor redemption requests, which is causing some challenges in the space. Not all private credit is created equal, just like not all borrowers are the same. Those that pledge ample collateral, have good income coverage to make payments, and have a stable job are a safe bet to lend money to, relative to someone with little assets and income. The private credit funds that are owned in portfolios at West Oak fall into the former category and aren’t facing the same challenges as some funds which have issued loans with light covenants and underlying fundamentals.

The increase in redemption requests creates opportunities for the more conservative fund managers who can take advantage of pricing dislocations where quality loans may have to be sold at a discount. This allows managers to buy strong assets at a better value, thereby enhancing the rate of return profile. There is a common sports analogy that ‘the best offense is a good defence’, which in the case of private credit, is exactly what we want and have. This careful approach is exactly what positions us well in times like these.

The Bottom Line

Comparatively, private credit has held up through the 2008 financial crisis, COVID-19, and the 2022 rate shock for the same reasons a well-underwritten, low loan-to- value loan typically holds up through downturns and dislocations like we are seeing today.

Owning thoughtfully chosen managers, like we have, who diversify carefully, do exactly what we hired them to do: generate high income (~8.5% currently) with meaningful downside protection, offering investors reasonable diversification, especially when coupled with traditional stock and bond exposures within portfolios.

As always, thank you for your continued trust. If you have questions about your portfolio or want to discuss strategy in more detail, we’re here to help.

Sincerely,

Andrew, Kelly, Justin & the West Oak Team

-

Cliffwater Direct Lending Index, December 2024 — Historical returns and credit losses.